What do we do now?

April 2025

The words destabilised and unbalanced inform our current view of the geopolitical, macroeconomic and investment landscape. The younger iteration of myself understood, from a purely theoretical perspective, the psychological and emotional anguish that comes with investing in global capital markets particularly during tumultuous geopolitical and economic environments. Needless to say, the past 18 years have well and truly converted a theoretical knowledge to a practical one. 15 September 2008 (the day Lehman Brothers declared bankruptcy), 9 March 2020 (the day Italy instituted a national lockdown) and now the 2nd of April 2025 were but some of the days where, as an investment community we were forced to come to terms with not knowing what comes next. In March 2020 Howard Marks of Oaktree capital, in his investment memo “What comes Next II” cited Harvard epidemiologist Marc Lipsitch, who said we usually make decisions based on “(a) Facts, (b) informed extrapolations from analogous experience and (c) opinion or speculation. But since there no applicable facts regarding a Covid pandemic and no analogous experience, we were left with only speculation”. In environments where historical global aliases come into question, the temptation is for investors to turn to speculation to inform our decisions. Our view at Cannon, is that anchoring on speculation leads to reactivity which ultimately destroys value.

The first few months of the new US administration have reignited those all too familiar feelings of uncertainty, self-doubt and that inevitable question of “is this time really different?”. As an investment fraternity, the collective we, expected the Trump administration to institute tariffs but very few of us anticipated the mechanism used to “calculate” tariffs and the magnitude of the tariffs or a least the initial tariffs before the 90-day pause. The philosophical basis for the tariffs has been the long-standing belief by President Trump that US trade deficits reflect scenarios where the US economy is being taken advantage of. The first quarter of new US administration has brought with it material policy uncertainty has which began to result in a reduction in consumer, business confidence and growth expectation.

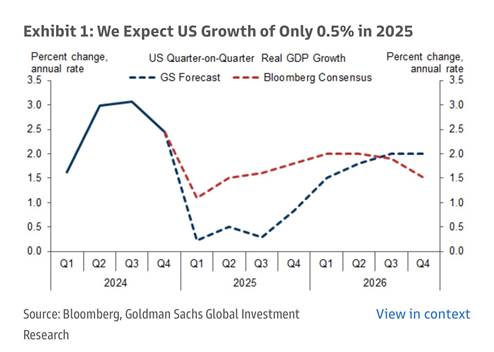

Chart 1

As a business and as individuals some of the best periods of absolute and relative performance have come from these periods of crisis and market turbulence. History has taught us that periods such as these require reflection, bravery and incorporating multiple possible outcomes in our assessment of the future.

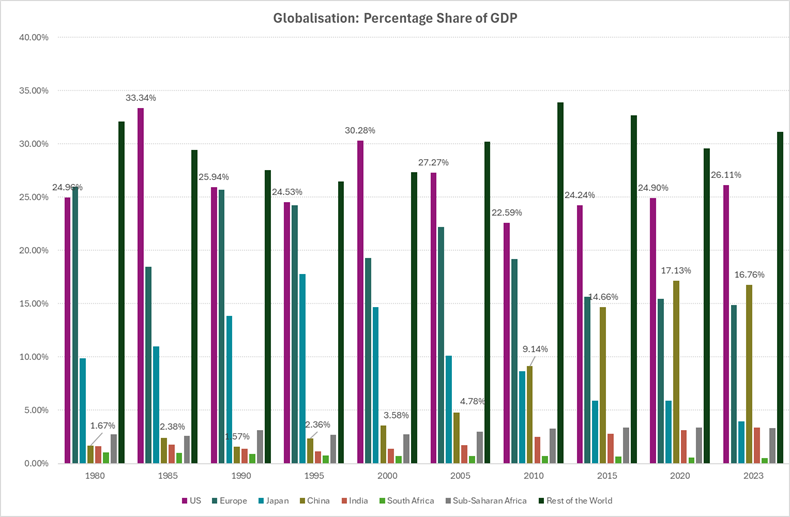

In taking a step back and reflecting, we subscribe to Professor Aswath Damodaran from NYU, thesis that the primary thematic drivers for economic growth globally of the last four decades have been globalisation (which has largely benefitted China) and the disruptive effects of technology, which has restructured the structure but ultimately benefitted of the US economy. Chart 2 showcases the benefits from globalisation China has experienced, increasing its share of global GDP from 1.67% in 1980 to 16.76% in 2023. Over the same period Europe and Japan, the biggest losers. One of the results of the consequence of the results of globalisation has been an increase in anti-globalisation sentiment reflected by election results in Europe and US. As a team, we have spent the last few years talking about the multi-polarity theme was likely to result in an increase in regional and global conflict, a decrease in nationalism, a decrease in globalisation and a structural increase in inflation. The tariff wars are a continuation of that theme, and the likely consequence is that non-US businesses that have the US as a sales destination will be disproportionately negatively impacted by tariffs and similarly US business with global supply chains or generating global revenue. There are typically three constraints for all governments ability to implement their agenda,

- Political capital

- Legislative and legal framework

- Markets

Thus far the only mechanism that has been somewhat effective in serving as a check and balance on the Trump administration’s economic agenda has proven to be markets. The US 10-year government bond yield increased from 4.0% of the 4th of April 2025 to 4.49% on the 11th of April 2025, putting significant pressure on the administration and resulted in the tariff pause. The oversight role of markets adds significant comfort to our outlook for markets.

There are some critical questions that need answering over the next few months and years:

- How does the trade war end where do the tariff rates end up?

- How does an increasingly isolated USA impact corporate America, particularly multinationals?

- Does the dollar remain THE reserve currency rather than A reserve currency?

- Does the Gold continue to benefit from the uncertainty?

- How do we navigate an environment where businesses representing over 60% of global market caps are domiciled and headquartered in a country with significant policy uncertainty?

- What are the new safe haven assets?

Chart 2

The coming weeks, months and years will assist us in answering these questions. In the interim the current market volatility has and will continue to present buying opportunities to acquire high quality companies that are well positioned to navigate the current macroeconomic environment. Our belief at Cannon is a fundamentals-based approach where each company, industry and country are assessed for their own investment merits, empowers us to navigate various investment environments. An informative illustration of the importance of a taking a methodical review of the possible impact of tariff at the company level is Crocs. We have been fans of the stock for some time, despite the internal arguments about the fashionability of their products. The business is a world leader in casual footwear for men, women and children. They have significant market share and industry leading profit margins, underpinned by the strong operational performance of their core business. On the face of it, Crocs is precisely the type of business the tariffs are intended to target, a US based business that produces ostensively all of its products abroad. Over 75% of Crocs products are made in either Vietnam or China. Theoretically, the tariffs will incentivise Crocs over the medium term to reestablish a significant manufacturing base for their product in the United States. It is worthwhile noting that over 44% of Crocs sales occur outside of the United States and this is by far the fastest growing segment of the business. Our anticipation is that countries with the highest US tariffs, will service the company’s international sales and those with the lowest tariffs supplying the US market in the short term. Will there be a material impact to the business? Yes, our projections are that the implementation of the tariffs as contemplated on “Liberation Day” would remove up to 20% of the value of Crocs. Despite the possible loss in value from the implementation of the tariffs, our belief is that Crocs presents significantly more value than the prevailing market price and we remain steadfast on our investment case for the business.

Beyond the US shores, we remain bullish on emerging market equities over the long term, with a particular preference to those businesses that have limited exposure to the US market as an export destination. South African equities are largely (not completely) insulated from the direct effects of the trade war given the limited non commodity supply to the US market. Having noted that, the trade war specifically between the world’s two largest economies will have a significant impact of global growth and the short-term operational performance of the businesses we are invested in.

We remain vigilant, cautious and opportunistic in our assessment of global capital markets.

Tshepo Modiba

Chief Investment Officer

Cannon Asset Managers