July 2025

At Cannon, we consider ourselves valuation-based investment managers. We base our investment decisions into stocks, sectors and countries, on the underlying fundamentals and mispricing opportunities presented. Our assessment of value is partially guided by our understanding of the prevailing macro-economic environment and long-term investment and geopolitical themes.

That term Globalisation again

Cannon Asset Managers has always leveraged academia to inform our investment philosophy, process and views. Our understanding on the current geopolitical landscape is no different. During the last few decades, human dynamics, global institutions, political relations and the global environment have become increasingly more intwined. While the increased global economic integration, forms of governance, the inter-linked social and environmental developments are often referred to as globalisation, there is no unanimously agreed definition

of globalisation - it means different things to different people. Depending on the researcher or commentator, it can mean the growing integration of markets, nation-states and the spread of technological advancements (Friedman, 1999); receding geographical constraints on social and cultural arrangements (Waters, 1995); the increased dissemination of ideas and technologies (Albrow, 1996); the threat to national sovereignty by trans-national actors (Beck, 2000); or the transformation of the economic, political and cultural foundations of societies (Mittleman, 2000). What is clear is that between 1990 and 2008 whatever your definition of globalisation is, globalisation increased in that period.

Unipolar, Bipolar, Multipolar

Over the last four years we have highlighted (possibly ad nauseam), the global geopolitical shift that has taken place from a unipolar international system that existed between 1990 until 2008, to a multipolar one. Post the USA winning the cold war, the country embraced and enforced their role as the prominent global superpower. An argument can be made that the “War on Terror”, the 2008 global financial crisis and the economic emergence of China, damaged the USA’s standing as the singular dominant geopolitical force. Since then, the transition into a multipolar world has taken shape. According to Vasconcelos (2008), the term multipolarity refers to “the emergence of a plurality of global actors, who limit the power of the US (United States) superpower and that of other ‘poles’ such as the EU (European Union). More specifically, it refers to the rise of China and India. Russia’s resurgence, and the growing importance of players like Brazil, particularly in international trade.” Academic literature tells us that unipolar geological periods are characterised by an increase in globalisation and a resultant decrease in inflation. These periods are also typically characterised by a reduction regional conflict, as the superpower adjudicates conflicts across the globe.

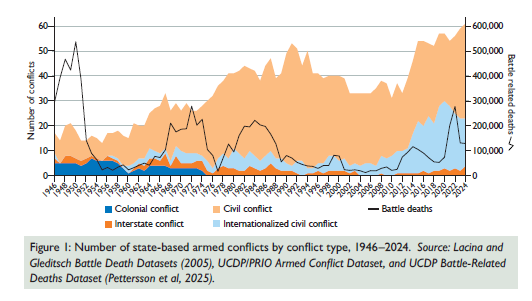

Chart 1 highlights that between 1990 and 2010, there was a decrease in global conflicts and battle related deaths. However, from 2010 to date there has been a significant increase in wars resulting in the highest level of conflict related deaths since World War II.

Chart 1 (Global Conflicts)

Inflation

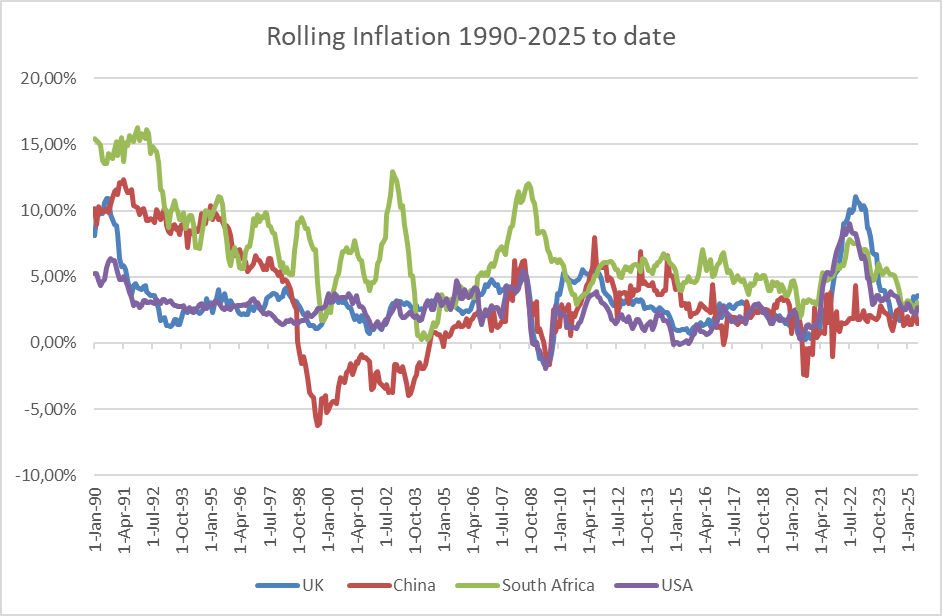

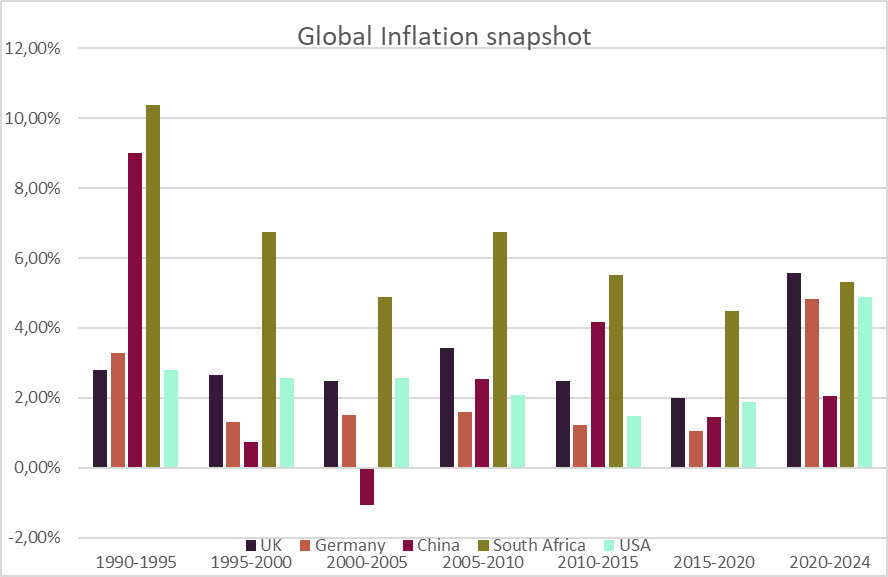

A snapshot of a basket of developed and emerging markets in chart 2 and chart 3, supports the thesis of price stability introduced by unipolarity. The countries included in the snapshot experienced a structural decrease in inflationary trends between 1990 and 2020. It is worthwhile highlighting that China experienced a deflationary period in the early 2000s, driven by the Asian Crisis. Chart 3 highlights that over the last 4-years, inflation has increased. In fact, 5 years on from the start of Covid and 3 years from the start of the Russia-Ukraine war, inflation remains above the targeted rate in countries such as the USA, Brazil, the United Kingdom, Korea and Japan. The increase has been driven by several factors including supply chain disruptions from the Covid pandemic. The remaining factors are largely associated with the realities of life under a multipolar world. Those factors include war and tariffs. Our belief is that a significant portion of the increase in inflation will be structural over the coming decade.

Chart 2 (Global Inflation)

Chart 3 (Global Inflation Snapshot)

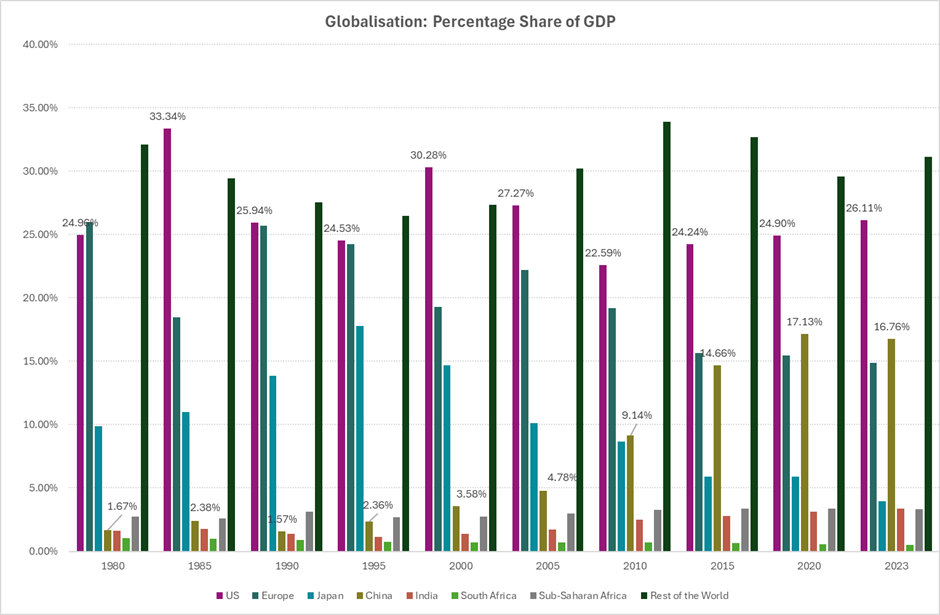

The relatively stable environment from an inflation and conflict perspective between 1990 and 2010 was ideal operating environment for many businesses. It allowed companies to optimise their operations based on location of headquarters, production and sales, which lead to widening operating margins and profitability. As highlighted in our, “What do we do now?” memo, the clear winner from the period of rampant globalisation has been China which has seen it’s share of global GDP increase from 1.67% in 1980 to 16.76% by the end of 2023. Over the same period Europe and Japan were amongst the biggest losers. Chart 4 shows the trend clearly, with the USA one of the few developed economies to maintain their global economic share by leveraging the transformative power of technology.

Chart 4

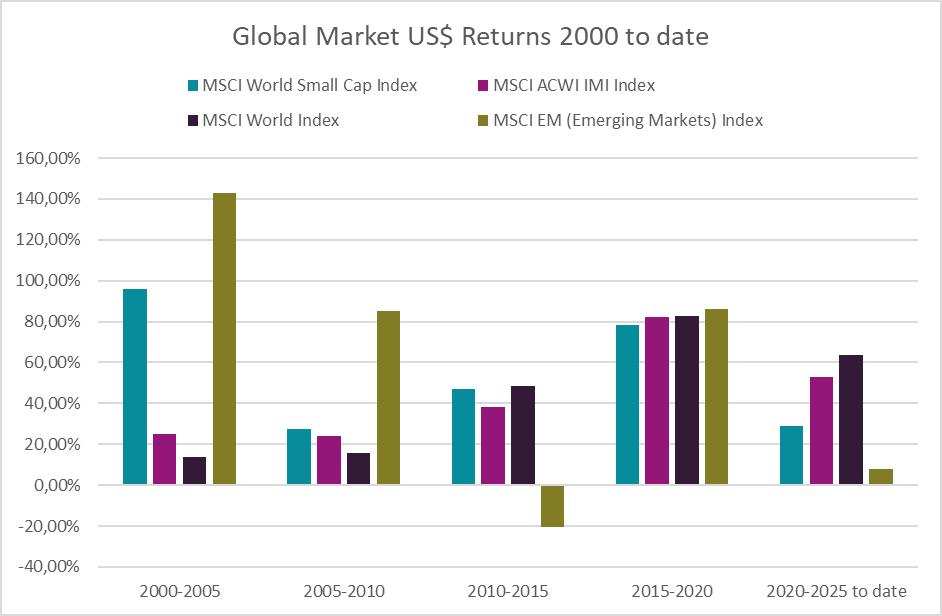

Up until the late 2010s the benefits of globalisation seemed to extend to emerging market companies broadly. Chart 3 and Chart 5 below showcase that up until 2010, emerging market equities outperformed the MSCI World and the MSCI All Countries Indices both of which are heavily skewed towards large cap developed market companies. Interestingly, Emerging Market equities have lagged their development market peers materially since 2010 (with the exception of the period 2015-2020 where there was parity).

Chart 5

The multipolar world has come with material changes in factors, that as an investment house, we had learnt to take for granted. Perhaps the most significant of these changes is that we can no longer take for granted policy certainty from the basket of developed economies. The US now has policy variability that has and will likely continue changing core economic principles and global allegiances based on election outcomes. We can no longer take the independence of the FED as a certainty. The European Union integration and continued existence was thrown into question by Brexit and subsequent commentary from increasingly prominent political parties and movements within various European nations. Coupled with these changes, we are navigating an investment environment with higher inflation, increased protectionism and more frequent prevalence of wars.

The world is truly in flux. The reality however is that even in the period of relative stability between 1990 and 2008, the winners at a continental, regional, country, industry and company level were not uniform. Successful investment decisions were driven by skill, discernment and intuition. As we navigate the period ahead, we will need those factors in bucketloads, as well as the ability to be agile in our decision making based on new structural changes.